Those of you who have done your research might understand the basics of how an NFT works, but there are still some questions that aren’t so clear. One of those questions is how do NFTs actually prove ownership?

NFTs prove ownership by showcasing immutable public transactions on the blockchain. The blockchain allows you to see who the creator is, the exact day and time it was minted, and the quantity. Even though someone could technically mint the same underlying asset, blockchain data expose these fakes.

When it comes to NFTs and ownership, there’s a lot to break down to fully understand how it all works. That’s exactly why I wrote this thoughtful article.

What Do You Actually Own When You Buy an NFT?

Before we get into how NFTs prove ownership, I think it’s important to clarify what you actually own when you buy an NFT. Keep in mind that there are still many gray areas when it comes to NFTs and any associated intellectual property. Hence why I’m laying it all out in the open here.

When you buy an NFT you are simply paying for the immutable proof of providence. That means you aren’t buying the underlying asset such as the image, video, or whatever it might be that’s connected to the NFT via its metadata. What you’re really buying is code on the blockchain that may or may not represent something else.

The common misconception is that when you buy an NFT you also own the underlying asset. From both a legal and technical standpoint, you don’t. You simply own code on the blockchain that states who, what, and when your token was created.

So why is that? It’s simple. According to the Copyright Review Board, only a person can be an agent in law.

That means artificial intelligence like smart contracts can’t enter contracts. Meaning if the creator of an NFT is utilizing smart contract technology to issue their holders’ copyright for their underlying assets, then it’s still unclear whether it’s legally valid or not.

That’s the gray area I’m talking about. After all, isn’t the point of owning an NFT to prove ownership of something else besides the NFT itself? To be honest, it really comes down to the creator of the NFT and their intentions.

For now, contracts agreed upon through NFT technology are about as legit as a handshake. For example, if you buy an NFT that promises you access to one conference every year for three years as long as you hold that NFT, the creator is not legally responsible to follow through with that agreement because the contract is on the blockchain, therefore it’s not technically a valid contract in the eyes of the law.

That’s not to say that you couldn’t create a legally binding contract to go along with the NFT, but there would be much more paperwork involved in addition to the NFT transaction.

In order for smart contracts to hold people accountable legally, the law would have to be changed. Eventually, I believe it will. We’re just not there yet.

So, What Ownership Do NFTs Prove?

NFTs prove ownership of the token itself. That is the digital code (such as the URI) that is published on the blockchain. Nothing more, nothing less. Utility and underlying assets aside, NFTs still authenticate who the creator is, when the token was created, and everything in between. That in itself could be considered valuable.

Say for example you buy an NFT from Snoop Dogg that links to his new album. On the blockchain, you can see that Snoop is the creator of the token and the exact time he created it—and that data can never be changed. So even though you really only own the token, that token will forever represent the album he released (on the blockchain).

It’s like buying a physical copy of Snoop’s album. Just because you own the physical copy of his album doesn’t mean you own the copyright to his work, it’s really just a representation of his work that you get to enjoy.

Moreover, if you have a physical copy of Snoop’s album and it’s signed, plus it comes with proof of authenticity, you could assume that particular album would be more valuable than others that aren’t signed.

That’s one of the main value points of an NFT. It’s an immutable representation of something else and is verifiable on the blockchain.

And remember, that’s not even considering all the other possibilities that come with the use of the technology. I know it can be hard to accept or to even see past the immediate future of NFT tech, but history has shown that great things take time.

A majority of people didn’t see any value in the internet or buying things online, yet, everyone who’s reading this has used the internet and has bought something online.

Do Fake NFTs Exist?

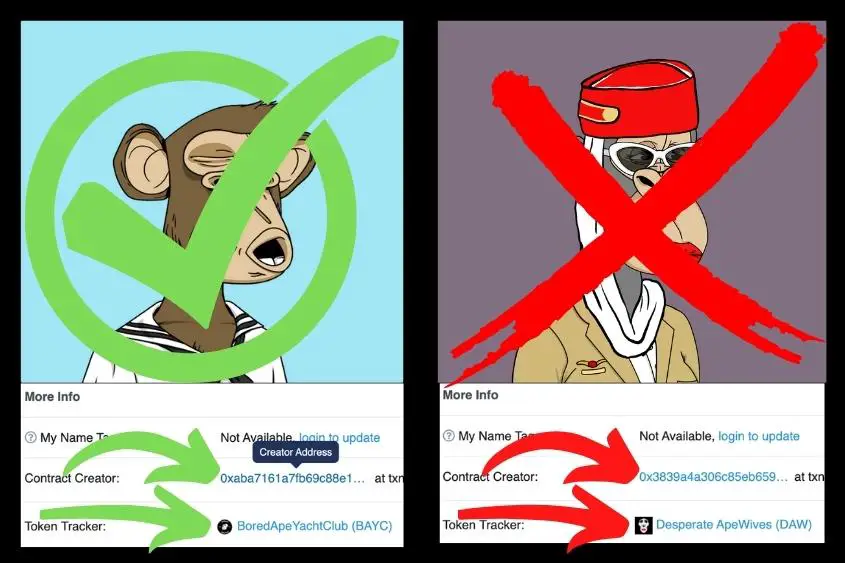

There is no such thing as a fake NFT. An NFT is one-of-a-kind and can’t be copied. However, the underlying assets could potentially be used to create an NFT look-alike, but the blockchain is able to quickly dismiss any copies via its immutable data and public ledger.

There’s no doubt that look-alike NFTs exist. Some of the most popular NFT brands like Bored Ape Yacht Club and VeeFriends have been replicated. But were the replicas ever as valuable as the real NFTs? No, because everyone is able to view the blockchain to see which collection is real and which is just a look-alike.

Furthermore, look-alike NFTs do not provide holders with the same perks as the authentic NFTs might. One example comes from the VeeFriends NFT collection. Holders of VeeFriends NFTs get access to one mega-conference per year, for the first three years of the tokens’ existence (2022-2024).

If you were to hold a look-alike VeeFriends NFT in your wallet, you wouldn’t gain access to the conference because the blockchain data is different. Hence, making the authentic NFT more valuable.

I know I mentioned contract agreements via NFTs aren’t legally legit, but that doesn’t mean creators and brands behind the NFTs aren’t committed to doing things the right way for their holders.

At this point in time, it comes down to the integrity of the person or brand to hold up their end of the deal when promising something through NFTs. Ultimately, their reputation is still on the line.

Imagine if 50,000 people bought a $500 NFT from Nike that promised them all a free pair of shoes within a year of purchase, but Nike failed to deliver on their promise. Don’t you think people would be upset? I know I would be.

As a result, the world would hear about it. So, not only would Nike lose the trust of those 50,000 customers, but they’d probably lose the trust of millions of people after the word had spread that they made $25 million ripping people off, potentially destroying the brand.

Do you see how that works? The blockchain provides transparency and enforces accountability by utilizing NFTs.

That’s also why it’s so important to research every NFT you buy and the reason why so many people have been scammed out of their hard-earned money buying NFTs. They buy false promises from brands with no reputation, who ultimately don’t care if their brand fails because they never had one to begin with.

How to Prove Ownership of Your NFT

NFT ownership is proven by accessing your wallet using your private key. Your private key is what controls the NFT, while the content creator’s public key serves as a certificate of authenticity for your particular digital asset.

When you purchase an NFT, the token is transferred to your wallet via your public address. That also means the creator’s public key is a permanent part of your token’s history, signifying its significance on the blockchain.

Below I explain how to prove ownership of any NFT on the blockchain in five simple steps.

1. Go to Etherscan.io.

Etherscan is the Ethereum blockchain explorer. You can view every transaction that has ever occurred on the Ethereum blockchain using Etherscan, as well as the contents of anyone’s wallet.

2. Enter the wallet’s public address into the search bar.

Enter the wallet address of whichever wallet you want to use to prove ownership of an NFT. You can copy the wallet address from your wallet if proving ownership of your NFT, or you can find someone else’s wallet address by searching for their username on Opensea.

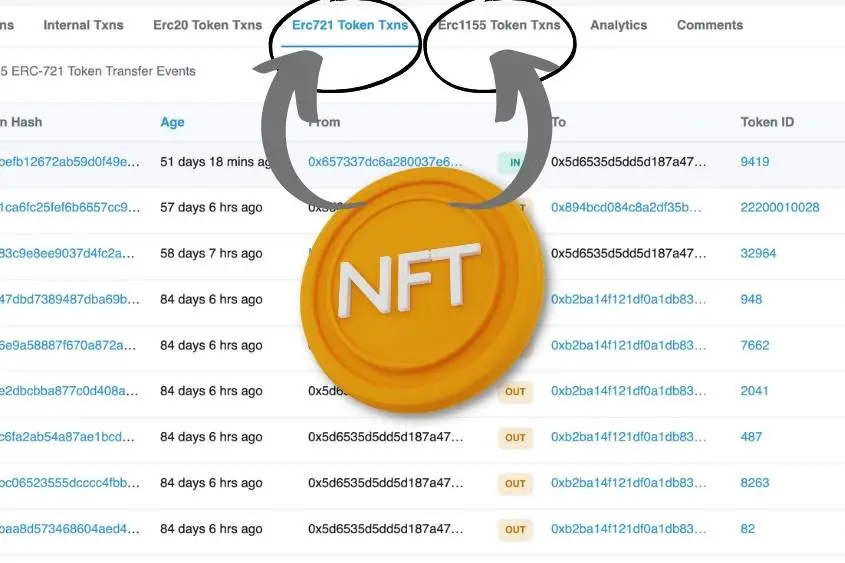

3. Scroll down to the Token Txns tab(s).

After you hit search, you will have the ability to view the wallet’s contents as well as every transaction that has ever taken place using that wallet’s address. To find NFTs, scroll down to Token Txns (Erc721, Erc1155, etc). These are a list of different types of NFT transactions.

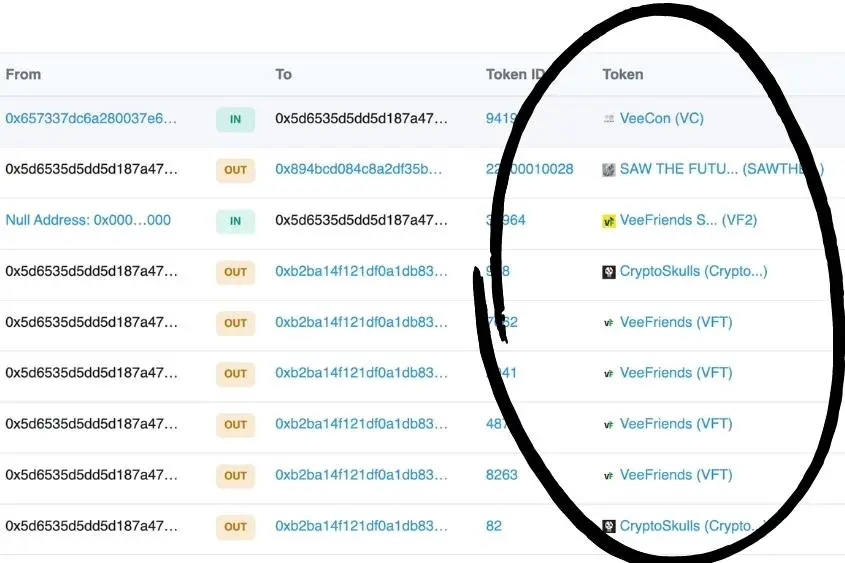

4. Find the token you want to view.

If you see IN, that means it was received into the wallet. If you see OUT, that means it was sent out of the wallet. Regardless of whether an NFT transaction shows IN or OUT, you can still find the current owner of the NFT under the Token section.

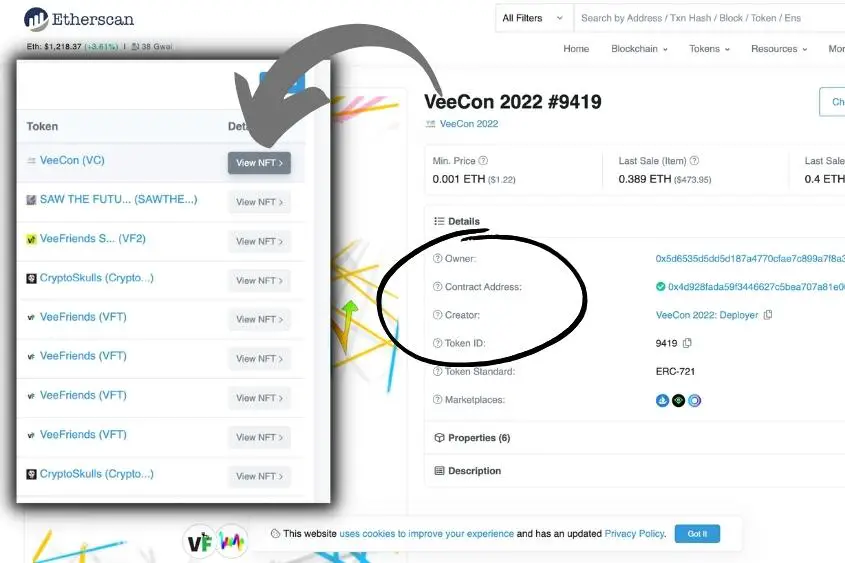

5. Select “View NFT”.

Once you find the NFT you want to prove ownership of, simply click View NFT. This will show you the current owner address, contract address, creator address, token id, token standard, the marketplaces it’s currently showcased on, the properties, and its description.

Though NFTs prove ownership of the token itself by utilizing the blockchain, the blockchain doesn’t necessarily prove ownership of any underlying assets associated with an NFT. For now, underlying assets have to be proven through traditional means like a copyright or another legally binding contract.

5 thoughts on “How Do NFTs Prove Ownership? A Thoughtful Explanation”

Comments are closed.