Advancements in technology always bring new terms, some of which can be hard to understand. Smart contract technology is one of these terms that we hear a lot about today, but we still struggle to wrap our minds around.

A smart contract is a set of promises, specified in digital form. It contains code that’s capable of automating the execution of an agreement’s terms and conditions so that all parties can be immediately certain of the outcome, without the need for an intermediary.

Smart contracts have been around for decades. However, more recently, the term has been thrown around more often with the development of Web3. Below we will discuss the evolution, components, benefits, and risks of smart contracts.

What Is a Smart Contract?

Nick Szabo, a computer scientist, legal scholar, and cryptography expert, is credited with developing the smart contract concept. He defines a smart contract as “A set of promises, specified in digital form, including protocols within which the parties perform on these promises.”

So, a smart contract is a computerized algorithm that carries out the contract’s terms. This definition, on the other hand, does not differentiate smart contracts from other well-known contractual forms that implement automated performance, such as vending machines.

Vending machines are self-contained automatic machines that dispense goods or offer services in exchange for coins or, in certain cases, credit card payments. Vending machines are programmed with specific rules that they follow.

If vending machines and smart contracts have no fundamental differences, smart contracts are as old as Roman law itself. Hero of Alexandria, a Greek engineer, and mathematician, documented the first vending machine in the journal Pneumatika in the first century CE. His machine dispensed holy water after accepting a drachma coin.

Smart Contract Evolution

Most of today’s legal contracts are created using word processing templates customized by attorneys and other legal professionals. They contain standardized legal language, such as manifest within a Word document, that specifies terms and conditions. They rely on third parties for interpretation and enforcement.

This is a time-consuming and redundant procedure. Furthermore, if problems arise, the contracting parties rely on arbitrators and the courts to resolve the matter. This is also time-consuming, difficult to predict, and expensive.

The smart contract—a computer program that can carry out the contract—is the solution. It contains code (e.g., Ethereum JavaScript Solidity) capable of carrying out an agreement’s terms and conditions.

In the same manner that a legal document would, the contract code describes the terms and conditions as a series of if/then/else syllogisms. RPC calls to other smart contracts or “off-chain” oracles can be used to validate and confirm the conditions. Smart contract code can then be automatically executed on the blockchain in this way.

Smart contracts will change the face of attorneys and legal professionals, who will be required to be skilled in both law and computer programming.

For example, a contract that automatically calculates the payments that are due and the goods to be delivered between the parties, and then automatically arranges for those payments to be made and the goods to be delivered, relies on software code.

If buyer Steve orders a piano of a specific brand, make, and year that becomes available through seller Rocky, Steve’s party pays money to Rocky’s party’s bank account, and the piano is delivered to Steve’s home, the contract terms are described in logic statements.

It is critical not only that the code is developed and tested, but also that it is written with security checks on the identity of the parties.

Smart Contract Components

There will initially be hybrid smart contracts developed with separate components on the blockchain and outside the blockchain, as the smart contract evolves. Smart contracts will eventually be on-blockchain-only components as blockchain technology evolves and becomes more widely accepted.

Here are some of the possibilities:

- Ethereum Solidity code is an example of smart contract code that is stored, verified, and executed on a blockchain.

- Smart legal contracts are a set of standards for using smart contract code as a complement or complete replacement for traditional legal contracts.

- An actual contract may start off as a smart contract with some off-chain logic and execution, but as the concept evolves, it will evolve into a fully blockchain-executed smart contract. Even the most basic contract can be entirely automated. Other contracts may include self-executing terms as well as terms that are not part of the software code. This is because, especially for complex contracts, not all decisions or steps in a contract can be reduced to logic statements.

A smart contract, in the eyes of DApp programmers, is just a well-written program that executes the contract, i.e., a contract written in code. They would say that all programs are, in fact, contracts.

The concept of a contract has a different meaning for lawyers. It requires the exchange of an offer and acceptance, as well as consideration and specific terms and conditions. They find it difficult to accept that a code can be made into law.

Smart Contract Benefits

Smart contracts, like any new technology, have advantages and disadvantages. The benefit of a distributed blockchain over depending on a single trusted central ledger is that it gives a more trustworthy ledger.

Participants and regulators benefit from increased security, traceability, and transparency of data and transactions, as well as lower operational costs, thanks to blockchain technology.

The use of smart contracts in combination with blockchain improves certainty, security, and resilience. Independent parties can verify the terms. Furthermore, because the information recorded on the blockchain is kept on numerous nodes, it is protected against security concerns.

Smart Contract Risks

Governance, deployment, risk management, regulatory, and legal issues are all potential risks associated with the use of evolving smart contracts and blockchain technologies. Market confidence in technology is fundamentally based on these risks and how they are managed.

In the parts that follow, we’ll go through them in greater depth. In order to ensure accuracy and trustworthiness, blockchain and smart contracts require standards or a set of common rules by which all participants operate.

When it comes to changing the rules, the decentralized model presents challenges because those changes should be agreed upon and accepted by all participants in order to function consistently.

To implement and operate blockchain as a legal application, a governance framework will be required, which will include oversight and monitoring functions, rule setting, and acceptance and change control management.

Governance will be required in general, not only for legal but for all information-management technology. This transformation to some common information governance rules is important not only for blockchain but also for other pursuits like e-discovery and cybersecurity.

Governance standards around the blockchain will contribute to market confidence in the technology and the legal and regulatory environment. This will accelerate the adoption and success of smart contracts.

Smart Contract Challenges

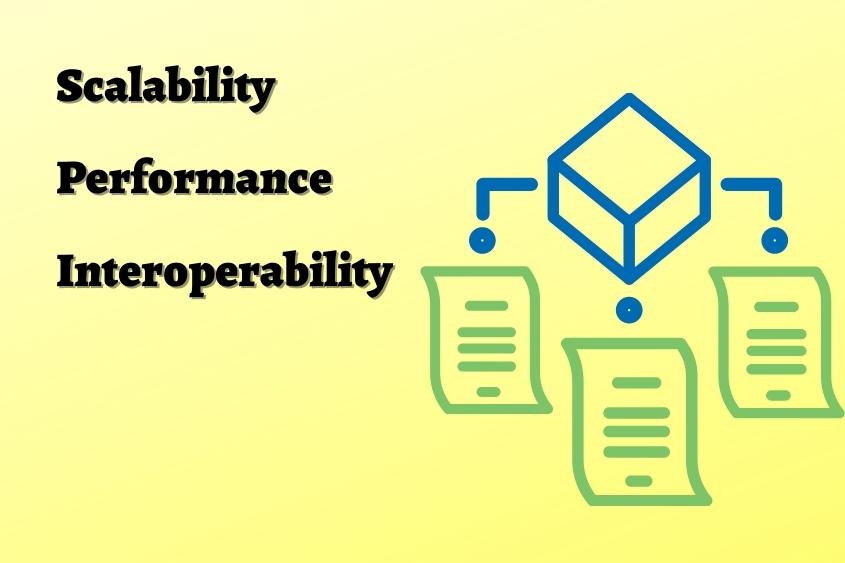

The success of blockchain will depend on whether it can be implemented practically and which applications are proper candidates. Briefly, the key deployment risks and challenges are listed below:

- Scalability – Each node in a blockchain network must be aware of every single transaction that occurs globally, which might slow down the network significantly. The goal is to make all transactions more efficient while maintaining the network’s decentralization and security.

- Performance – The computing resources and performance required for transaction processing, validation, and fraud detection will determine which banking, financial, and payment services can best be applied. At the moment, most blockchains are not capable of handling thousands of transactions per second. It will be limited to asset transfers that are not time-sensitive, such as the purchase or sale of a highly traded and volatile security.

- Interoperability – Ensure that different blockchain implementations can communicate with one another by ensuring interoperability. What would it cost to accomplish that? The alliance groups, who will ideally set standards, will determine this.

Smart Contract Legal Challenges

Smart contracts can raise a number of intriguing and challenging legal issues. For starters, has a legally binding contract been formed?

As previously stated, the current hybrid form of a smart contract mixed with a standard nonprogrammed or manual contract, such as a Word document with terms and conditions, raises some new validity concerns.

The legality of a smart contract is determined by a variety of factors, including the use case, the type of smart contract employed, and the applicable law.

Delaware and Arizona, for example, have passed legislation recognizing smart contracts.

In 2017, Arizona passed HB 2417, which includes a very specific definition of blockchain technology as a “distributed, decentralized, shared, and replicated ledger, which may be public or private, permissioned or permissionless, or driven by tokenized crypto economics or token less,” in order to avoid any legal uncertainty surrounding blockchain transactions and smart contracts relating to certain digital assets.

Smart contracts are described in HB 2417 as an “event-driven program with the state that runs on a distributed, decentralized, shared, and replicated ledger and can take custody of and instruct transfer of assets on that ledger.”

States that are ahead of the curve, such as Delaware and Arizona, have passed legislation to encourage blockchain development in their respective states. However, in many jurisdictions, the electronic nature of smart contracts is unlikely to be a barrier to contract formation.

The legal requirement of “certainty” might not be satisfied easily, as not all smart contracts operate in conjunction with natural language contract terms.

How will the parties to a smart contract get notice of its terms and conditions? When will they get to see those terms, prior to or after the smart contract is agreed upon and executed? How will we address those contracts that are required by law to be in writing? Is computer code considered writing? How do we deal with the formal execution requirements for deeds, i.e., in writing and signed by specified individuals or roles?

There are a variety of smart contract models to choose from. On the one hand, there are proponents of the “code is a contract” approach. Others, on the other hand, consider smart contracts to be the digitizing of business logic, such as payment, which is already taking place and may or may not be connected with a natural language contract.

A number of variations are likely to arise in the space between these two extremes, such as a “split” smart contract model in which normal language contract terms are linked to computer code via parameters.

Smart contracts can give rise to legally binding contractual interactions under the laws of a number of significant contracting jurisdictions, although there are jurisdictional differences.

Depending on the jurisdiction, the answer may differ significantly. In many jurisdictions, certainty about what constitutes contractual terms and whether they are comprehensive enough is a significant aspect in establishing the formation of a legally valid contract. Smart contracts that only digitize a process but do not contain or work in conjunction with contractual terms may not meet these requirements.

- Enforceability – When a smart contract has a legally binding contractual effect, the technology used to implement it may occasionally cause issues with legal enforceability. If a conflict arises, there may be no central administering authority to resolve it. Enforceability and jurisdictional differences could be addressed through dispute settlement methods. It will be pro forma to include a dispute resolution mechanism in a smart contract to address issues like enforceability and jurisdictional variations.

- Transparency – Transparency is possible with blockchain. But what if the parties don’t want the information shared? How do you keep parts of the contract private and retain the other benefits of blockchain?

- Changes – How can you unwind transactions that shouldn’t have happened—for example, if there was duress—or a contract that is illegal or in violation of regulatory rules for some reason (or somewhere)? On the Ethereum platform, this has already happened, with a technical “hard fork” solution (a split in the blockchain where non-upgraded nodes cannot validate blocks created by upgraded nodes following new consensus rules).

- Liability for mistake, error, or fraud – Where can someone seek compensation if something goes wrong with the contract’s execution, and they take a loss? We’ll need a technologically advanced court system. The courts have begun to identify blockchain as a tool for improving the administration of justice, not just for cryptocurrency. Courts will need to be able to work with blockchain evidence in the same way they have worked with e-discovery.

- Coding limitations – Contracts often deal with the unknown and have clauses that aren’t easily reduced to code or that can be executed automatically as a simple “if this, then that” procedure. Force majeure is a good example. Contracts often include concepts of subjective judgment, reasonableness, and acting in good faith. These concepts can not currently be readily translated into logic statements. That said, there will be code services that can provide “reasonability” tests, which have been used in securities trading for years.