Oftentimes, NFTs have been perceived as a piece of art or simply an image on a screen. If NFTs are simply just a JPEG, why is it that they utilize blockchain technology?

NFTs use blockchain technology to verify authenticity, prove ownership, and for smart contract integration. Without the blockchain, NFTs wouldn’t exist. NFTs store a lot of data—and since the blockchain is a digitally distributed, decentralized, public ledger, the two go hand-in-hand.

Although different blockchain networks utilize different types of smart contracts, the reason NFTs need blockchain technology to function remains the same.

Why Do NFTs Use Blockchain Technology?

You won’t understand NFTs with an internet mindset. That’s why you must know how blockchain technology is used in accordance with NFTs. A blockchain is a digitally distributed, decentralized, public ledger. Allow me to break down each of these terms individually to help paint the bigger picture.

Digitally distributed is the delivery of content—in this case, transactions—that are handled through a digital distribution platform (the blockchain).

Decentralized means that something (the blockchain) is controlled by multiple entities as opposed to a single entity, such as the case with Google. Why is that important? Well, if Google wanted to shut down today, that means all of us would lose the ability to use their platform. But with the blockchain, the network is shared across multiple computers, so there’s no single entity controlling it, rather it’s a diverse web that is supported by many people.

Public ledger is just that—a collection of accounts and transactions that can be viewed by the public. Your bank account is an example of a private ledger—only you can see your transactions and your account number. The blockchain, however, can be seen by anyone. That means I can go to your account, see all of your transactions, and even see what assets you currently hold or held in the past, along with who you sent them to. This public ledger creates a transparent network for people to transact on.

Non-fungible tokens (NFTs) are one-of-a-kind digital identifier that represents, verifies authenticity, and proves ownership of other assets—hence they live on the blockchain.

You see, the blockchain gives NFTs their power. It is the force behind an NFT. If NFTs lived on the internet, then you could easily screenshot an NFT, and you’d have no way to verify the authenticity or prove ownership. With blockchain technology, you can see who owns an NFT, who created it, and whom it has traveled between from the time of its creation. This is why NFTs use blockchain technology.

What Is the Most Used Blockchain for NFTs?

Ethereum is the most utilized blockchain for NFTs. The reason being is that Ethereum is extremely-secure and utilizes a robust data architecture. A majority of NFTs operate as ERC-721 tokens—which is the current standard for NFTs on Ethereum.

Ethereum has earned its spot as the top blockchain for NFTs. It was originally launched in 2015, then in 2016, a blockchain split occurred as a result of a hack in the original Ethereum network. This split was performed to keep Ethereum secure and is one of the reasons it remains the preferred NFT blockchain today.

Furthermore, as blue-chip NFT brands like Bored Ape Yacht Club and VeeFriends (along with other reputable brands like Adidas and Bud Light) continue to successfully distribute their NFTs using the Ethereum blockchain, the network has only gained more momentum from the community. As a result, Ethereum continues to foster even more trust.

That’s not to say that Ethereum is the only blockchain network that supports NFTs.

Which Blockchains Support NFTs?

There are numerous blockchain networks that currently support NFT smart contracts. Some options might be better than others, but ultimately it depends on your goals and situation. Below, I will walk you through a number of blockchains that currently support NFTs.

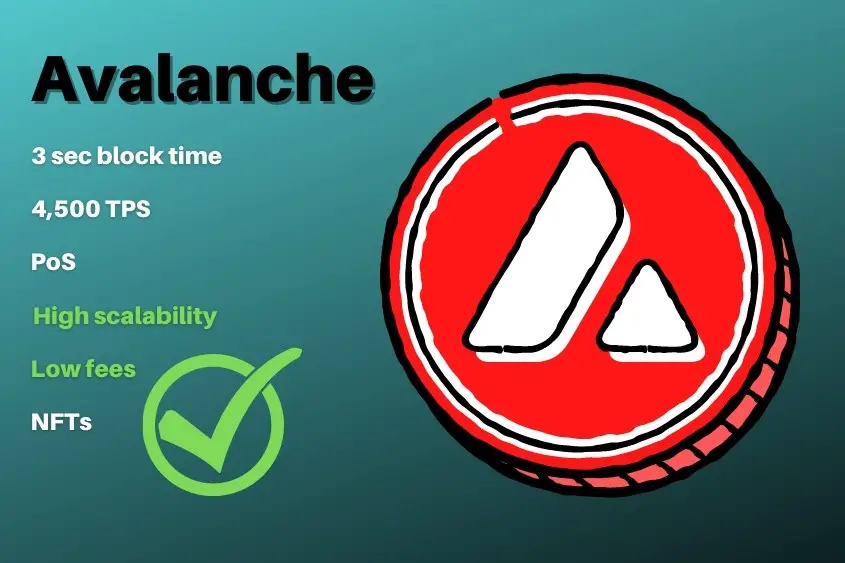

| Blockchain Stats | Ethereum | Solana | Avalanche | Cardano | Tezos | Polygon |

|---|---|---|---|---|---|---|

| Block time | 12 sec | 400 ms | 3 sec | 20 sec | 30 sec | 2.3 sec |

| Transactions per second (TPS) | 13-15 | 3,000 – 65,000 | 4,500 | 250 | 40 | 7,200 |

| Programming language | Solidity, Vyper | Rust, C+, C++ | Go, TypeScript, JavaScript, Python, Vue | Plutus, Marlowe, and Glow | Michelson LIGO | Golang |

| Consensus mechanism | PoW | PoH, PoS | PoS | PoS | LPoS | PoS |

| Scalability | Limited | High | High | Medium | Medium | High |

| Fees | High | Low | Low | Low | Low | Low |

Ethereum

I’ve already spoken for Ethereum, but it’s only right to include it in the list. Ethereum is the number one blockchain (both in sales volumes and its capabilities) that currently supports NFTs.

Ethereum is considered to be the OG of NFT blockchains. With that, there is no lack of activity when it comes to Ethereum. With Beeple’s $69 million sale of his NFT art; Beeple’s Everydays: The First 5,000 Days, it’s safe to say that there are some serious investors and creators participating on this blockchain.

Even though Ethereum is the obvious choice for many investors and creators, that doesn’t mean that it comes without any cons.

Ethereum is secure, trustworthy, and has a lot of potentials. However, it is also inefficient, boasting an average transaction time of 15 seconds at a rate of only 12 to 15 transactions per second (TPS). Plus it’s quite expensive to transact on, ranging anywhere from $15 to $150 per transaction. Even with its list of cons, a majority of people still choose Ethereum as their preferred NFT blockchain.

Not to fear though, Ethereum is in the process of upgrading the network from a proof of work (PoW) mechanism to proof of stake (PoS). This upgrade aims to bring Ethereum into the mainstream to make it more scalable, secure, and sustainable. The upgrade is said to increase the TPS significantly to around 100,000 TPS and reduce gas fees.

Solana

Solana has established itself as another good option for buying, selling, and creating NFTs. Solana is known for its fast, secure, scalable, decentralized apps and marketplaces. The network currently supports 65,000 TPS and 400ms Block Times.

Moreover, Solana provides users with a much more affordable transaction price compared to Ethereum, averaging less than $0.01 per transaction.

Also unlike Ethereum, Solana already uses a more efficient consensus mechanism(s) which results in its lightning-fast transaction speeds. Using a combination of proof of history (PoH) and proof of stake (PoS) mechanisms, Solana is currently one of the quickest and cheapest NFT blockchains available.

Solana also enables the creation of complex NFT markets. So far, NFTs may be purchased and sold on Solana-powered platforms such as Solanart.io, DigitalEyes.market, Solsea, and Metaplex.

Avalanche

Avalanche is an Ethereum Virtual Machine (EVM) compatible NFT blockchain with smart contract capabilities. It focuses mainly on interoperability, scalability, and usability. The Avalanche blockchain is often referred to as Ethereum’s rival blockchain, due to its smart contract capabilities.

The Avalanche network delivers a scalable blockchain while still maintaining decentralization and security, and emphasizes lower transaction costs, quick transaction speeds, and being environmentally friendly.

Avalanche is powered by its native token AVAX and several consensus mechanisms. The cool thing about Avalanche is that you can use your MetaMask wallet, which also works with many other blockchains like Ethereum, or you can create a wallet directly with Avalanche through their website.

Even though Avalanche is a few years younger than Ethereum and not quite as established, it does appear to be a promising NFT blockchain.

Cardano

Cardano is an NFT-capable blockchain created by Ethereum co-founder Charles Hoskinson. This blockchain runs on a proof of stake mechanism. This sophisticated blockchain enables developers to build highly scalable applications.

Technically speaking, there are two layers to Cardano. The Cardano Settlement Layer (CSL) is used for transferring ADA between accounts and recording transactions, and the Cardano Computation Layer (CCL) comes with the smart contract logic used by developers to move funds.

Fees on Cardano are low compared to other NFT blockchains, making it much less expensive to mint NFTs on its network, especially if you are creating a large collection or buying multiple NFTs.

Tezos

The Tezos blockchain is another popular network when it comes to NFTs. Similar to Cardano, Tezos utilizes a proof of stake mechanism, enabling 40 TPS. Although this is quicker than Ethereum, there is still room for improvement.

Tezos is special in that it has the ability to self-amend via on-chain mechanisms that are used for proposing, testing, selecting, and activating its protocol. This is different from other blockchains where the decisions are often made by a small group of individuals.

Another pro regarding Tezos is that users can create smart contracts. Smart contracts in Tezos are unique as they are written in the Michelson language. This language is different compared to other smart contracts.

“A Michelson program is a series of instructions that are run in sequence: each instruction receives as input the stack resulting from the previous instruction, and rewrites it for the next one. The stack contains both immediate values and heap-allocated structures. All values are immutable and garbage collected.”

Ultimately, Michelson allows Tezos’ smart contracts to operate securely.

Polygon

Polygon is different from all the previous blockchains mentioned. It is what’s called a Layer 2 solution built on the Ethereum blockchain. The great thing about Polygon is that it supports all the same tools Ethereum developers are accustomed to, while also reducing transaction fees and increasing speed.

To accomplish such efficiency, Polygon performs its transactions off of the Ethereum mainchain, and instead, utilizes sidechains. This feature allows users to mint NFTs for free, but still, many Polygon NFTs don’t sell for much money.

Although Polygon is cheap, scalable, and inherits some of Ethereum’s security—it’s not as secure as the Ethereum mainchain. That’s not to discredit Polygon though. Many users who are new to the NFT space enjoy its free minting capabilities and low-cost NFTs.

Similar to how social media platforms rely on the internet, NFTs rely on the blockchain. The blockchain can exist without NFTs, but NFTs can’t exist without blockchain technology.

Because the blockchain is a technology that facilitates digital exchange and units of value, it allows NFTs (proof of digital ownership) to exist. Ultimately, the two go hand in hand.

4 thoughts on “Why Do NFTs Use Blockchain Technology?”

Comments are closed.